Budgeting has helped me make sure I don’t spend money I don’t have and helped me make sure I set aside the money for my bills, making sure my bills were paid on time. Budgeting has been a significant help to me through tough times when income was low. With the basic understanding of how a budget works, you will have better control and awareness of your finances. You may also find you have more money than you thought!

What is a budget?

A budget is a breakdown of the amount of money that you have and how you intend to spend that money. Generally budgets are set on a month to month basis, taking into account your income (money in) and anticipated expenses (money out). Anything you intend to spend your money on, should be included in your budget. A budget is your way of telling yourself how you are going to be spending your money for the month. A budget is a tool to keep you on track and informed of your money habits.

The goal of the budget is to make sure you know where ALL of your money is going! By budgeting you can find out if you are overspending on things like eating out or shopping for unnecessary things.

Budget Example

I am going to walk you through how I have been setting up my budget for the last 4 years. It has honestly helped me find where I can cut back on my spending to help me save money!

Write out all of these essential items in your budget first!

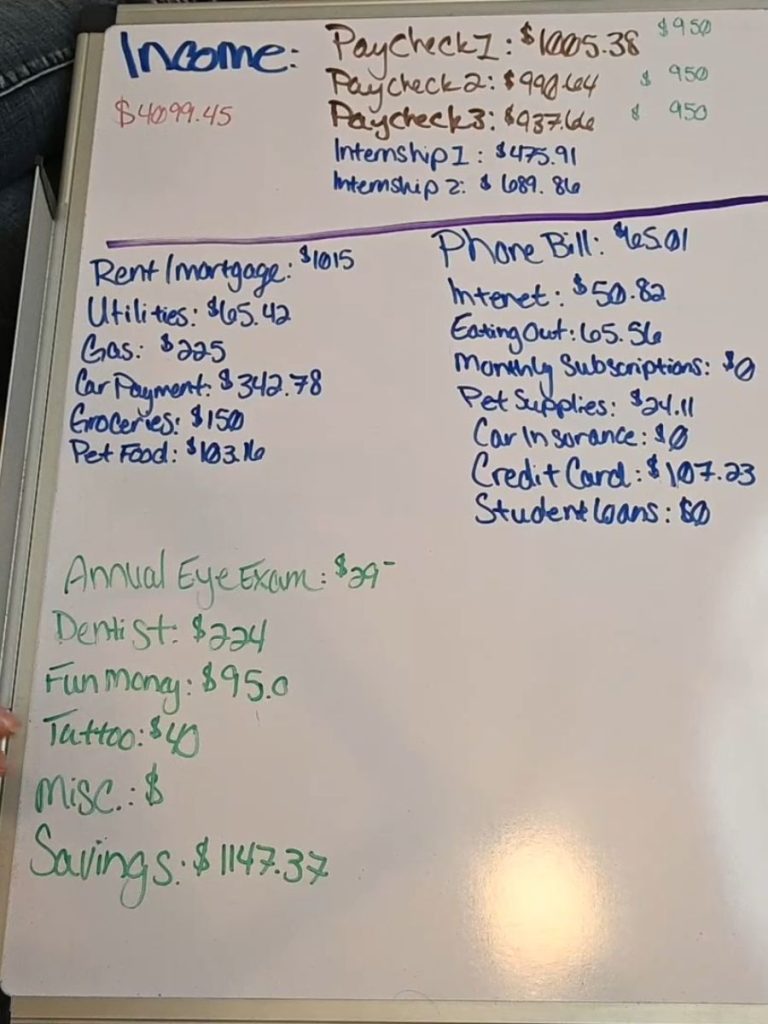

Your budget should start with the following essential information:

- How much money will you receive each paycheck? And how many paychecks do you expect to receive that month.

- Paycheck 1 – $1005.38

- Paycheck 2 – $990.64

- Paycheck 3 – $937.66

- Internship 1 – $475.91

- Internship 2 – $689.86

- Monthly Total: $4099.45

- What essential bills do you have?

- Rent/Mortgage – $1015.00

- Utilities – $65.42

- Gas for your car – $225

- Groceries – $150

- Life essential prescriptions $0

- Pet food – $103.16

I say put these first because they are essential for shelter, transportation, and food! For both you and your loved ones.

Once I know I have funds to feed myself and pay for rent, I then write down other bills and expenses.

Other bills/expenses:

- Phone Bill – $65.01

- Internet – $50.82

- Car payments – $342.78

- Eating Out – $65.56 (estimate or set a limit for yourself)

- Monthly Subscriptions – $0

- Pet supplies $24.11

- Car insurance $0 – I paid in 6 month installments

- Credit Card payments – $107.23

- Student Loan payments – $0 (deferment while in school)

- Other Prescriptions $0

Next, I budget for excess things (generally estimates or limits set by you)

Miscellaneous/non essential

- Annual Eye Exam – $29.00

- Dentist – $224.00

- Fun money for date night or a friends night out, etc – $95.00

- Tattoo Money – $40.00

- Miscellaneous: random things that you don’t often think of but you need like dishwasher detergent, toiletries, napkins, feminine products etc. – $57.47

- Savings – $1417.37

Your budget will not look exactly like mine. This set up should give you the foundation to start setting up your own budget! Your expenses may be different than me, you may have a different life situation and tailor your budget accordingly.

The above budget my budget from several years ago while I was working a full time job, going to school part time and working an internship 30 hours a week. Having a budget helped me make sure I was managing my money correctly. I was essentially working two jobs for roughly eight months. I knew the internship was going to end and I didn’t want to start living a lifestyle I couldn’t afford once I lost the extra income. To prepare I budgeted to save as much of my extra income as possible. This set me up for when my income dropped again.

You can and should update your budget as often as you need. Example: if you estimated that you were going to spend $150 on gas this month and you learn that you are going on a road trip you will need to adjust your budget. Also, if you find that adjusting your gas budget puts you in a deficit you either need to reduce your spending elsewhere or you need make up the extra cash needed for gas.

I also encourage you to give your budget some excess padding. Meaning, I usually slightly overestimate how much money I spend on gas to account for fluctuating gas prices. I always have a little bit of money budgeted for my miscellaneous category for random things that I don’t often think of like dental floss, deodorant, or new socks. Additionally, I leave about $100 left un-budgeted just in case there is a larger unexpected expense.

Questions

What if my paychecks vary from paycheck to paycheck?

I would either use the average of your last couple of paychecks or calculate your potential earnings based on: hours worked x hourly pay x avg tax % deductions (example: $14 x 35hrs x 20%). You can calculate your average tax % deductions by looking at your previous pay stubs to figure out what percentage is taken out every payday.

How do I estimate how much gas I am going to need to pay for?

What I have done in the past is look at how much money I spent in previous months when I was driving far more often. Fluctuating gas prices can cause a bit of an issue and if you like to take longer spur of the moment car trips your gas needs will also go up.

How often should I check in with my budget?

I recommend checking in with your budget vs your spending at least once a week. I personally reference my budget and spending several times a week, to keep myself from getting overwhelmed trying to catch up on my transactions.

What about retirement?

Currently the only retirement I have set up is through my employer and I have a percentage taken out automatically. This ensures I am always putting money away in retirement and I never see it, so I don’t miss it and I don’t have the opportunity to choose whether or not I want to put into retirement or something else.

Can I put anything in my budget?

If you are going to spend money on it, it should be in your budget. Getting a tattoo, have it in the budget. Have a medical procedure? Have it in the budget. Getting a refund from somewhere? Have it in the budget.

Leave a Reply